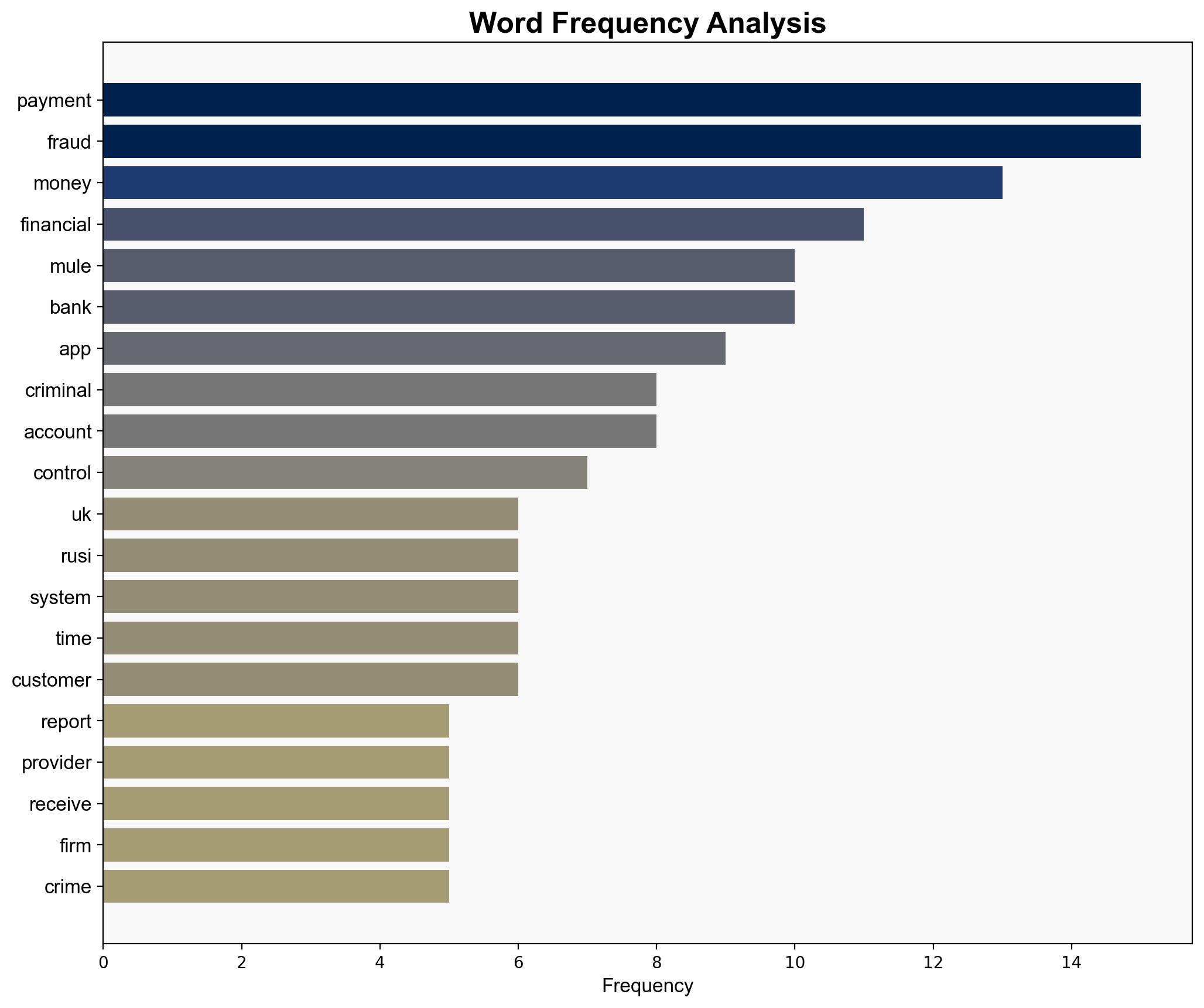

Authorized Push Payment Fraud a National Security Risk to UK Report Finds – Infosecurity Magazine

Published on: 2025-08-15

Intelligence Report: Authorized Push Payment Fraud a National Security Risk to UK Report Finds – Infosecurity Magazine

1. BLUF (Bottom Line Up Front)

The most supported hypothesis is that the growth of small payment service providers (PSPs) and digital banking platforms, with inadequate financial crime controls, significantly contributes to the rise of Authorized Push Payment (APP) fraud in the UK, posing a national security risk. Confidence level: High. Recommended action includes enhancing regulatory oversight and fostering real-time collaboration between financial institutions and law enforcement.

2. Competing Hypotheses

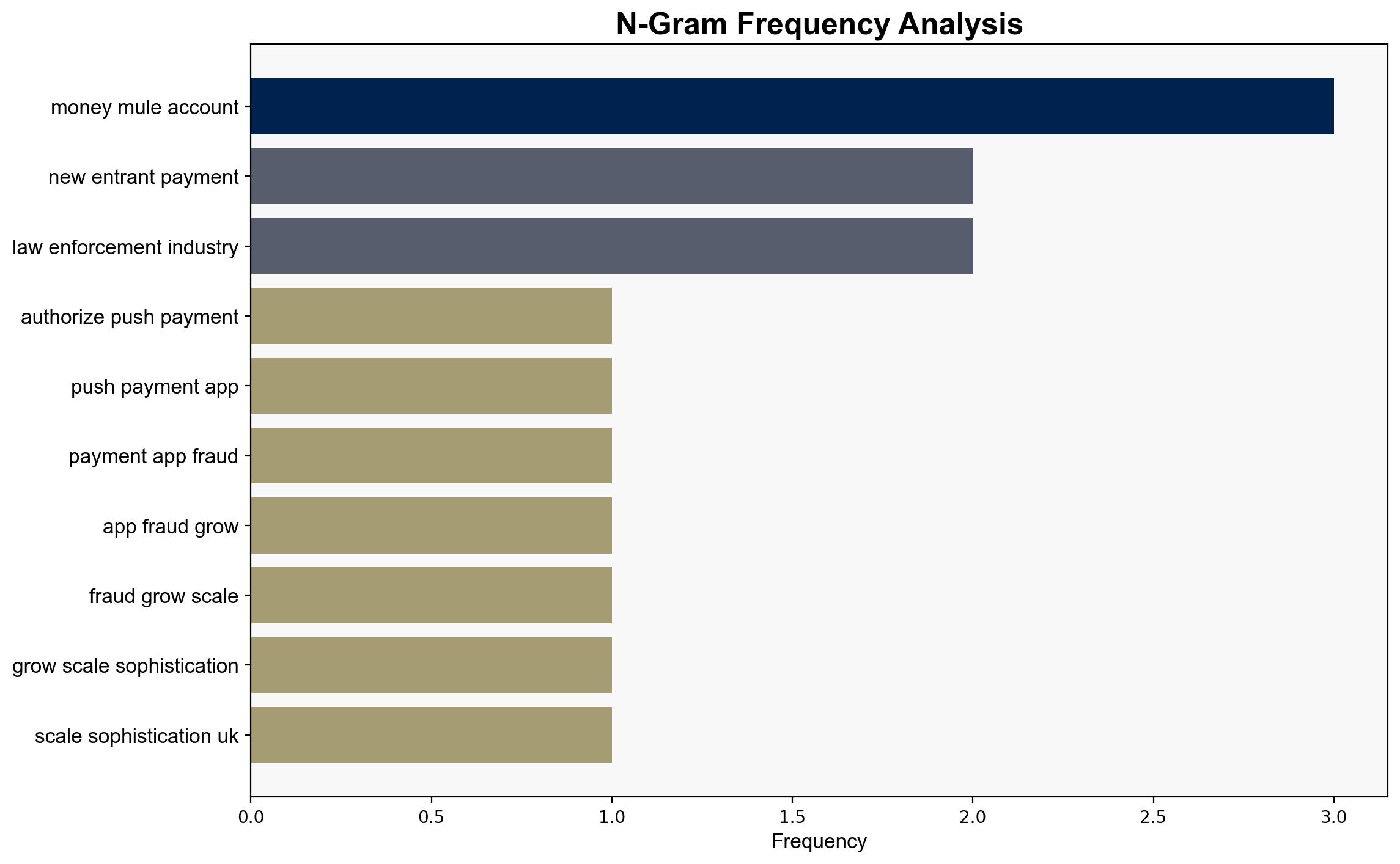

Hypothesis 1: The proliferation of small PSPs and digital banks with weak financial crime controls is the primary driver of APP fraud, making it a national security threat.

Hypothesis 2: The rise in APP fraud is primarily due to sophisticated social engineering techniques and the use of AI by organized crime groups, independent of the growth of small PSPs.

3. Key Assumptions and Red Flags

Assumptions:

– Hypothesis 1 assumes that small PSPs inherently lack robust financial crime controls.

– Hypothesis 2 assumes that technological advancements in social engineering are the main enabler of fraud.

Red Flags:

– The potential underestimation of the role of large financial institutions in facilitating fraud.

– Lack of detailed data on the proportion of fraud attributable to small PSPs versus larger banks.

4. Implications and Strategic Risks

The increasing sophistication of APP fraud could lead to significant financial losses, undermine trust in the financial system, and potentially fund organized crime and terrorism. The rapid evolution of fraud techniques, including AI-driven attacks, poses a continuous threat that requires adaptive and proactive measures.

5. Recommendations and Outlook

- Enhance regulatory frameworks to ensure small PSPs implement robust financial crime controls.

- Promote industry-wide real-time data sharing and collaboration to detect and prevent fraud.

- Scenario Projections:

- Best Case: Comprehensive regulatory reforms and industry collaboration significantly reduce APP fraud incidents.

- Worst Case: Continued rise in fraud due to inadequate controls and evolving criminal tactics, leading to severe economic and security repercussions.

- Most Likely: Incremental improvements in fraud prevention, with ongoing challenges due to evolving criminal methodologies.

6. Key Individuals and Entities

Jonathan Frost, Monzo Bank, Royal United Services Institute (RUSI), Financial Conduct Authority (FCA).

7. Thematic Tags

national security threats, cybersecurity, financial crime, regulatory oversight, digital banking